Insurtechs are the new kids on the block that are disrupting the traditional insurance industry. Inspired by a current project we are working on with an insurance client, we take a broad overview of the insurtech industry, its development and its influence on the insurance industry. We also look at some examples of insurtech companies with greatcustomer experience that you can draw inspiration from.

Tl;dr

- What is insurtech?

- The rise of insurtech

- Where insurtechs are now

- What this means for traditional insurance companies

- Insurtechs with superior user experience

- You’re an insurer. Do you need a mobile app?

The insurtech industry

What is insurtech?

Investopedia refers to insurtech as the “use of technology innovations designed to squeeze out savings and efficiency from the current insurance model”. Others define the terms as constantly changing technologies used in the insurance industry. And while being technology-led is what distinguishes insurtechs from traditional insurers, what makes them stand out is the dedication to an intuitive digital-first approach and simplified claims handling and settling processes.

The rise of insurtech

To understand how insurtech rose to power, we can take a look at the ‘fintech story’ and draw parallels. Most fintechs began as startups, operating with much lower cost burden because they don’t have to deal with brand networks and legacy systems. By developing innovative digital products at a fast pace, they managed to enter a market that was traditionally dominated by large banks. The story of insurtechs is pretty much the same. Both insurtechs and fintechs were welcomed by digitally-savvy customers, while they both skipped some of the heavy regulatory frameworks that applied to incumbents.

Where insurtechs are now

Over the past few years, insurtechs have grown by leaps and bounds - according to Reuters, global investment in insurtech startups totalled $10.5 billion in the first nine months of 2021, a record high level for the period. In comparison, the global insurtech funding for the whole of 2020 was $6.9 billion. Over this same period, the most successful insurtech ventures started moving beyond the seed and venture capital rounds of financing to advanced funding models and rounds.

The online channels and digital technologies of insurtechs are perfect for younger generations who are less company-loyal and value convenience and speed most of all. For the digital-savvy, receiving insurance quotes or submitting claims is always preferable to an office visit.

What this means for traditional insurance companies

Traditional insurers should clearly keep an eye out for insurtechs - they might be in their early days but they are already impacting the industry. Many traditional insurance companies have started paying much more attention to newcomers and are looking for ways to partner with insurtechs through joint ventures, limited partnerships or long-term contracts. Others are seeking and analysing best practices for insurtechs and trying to tackle them in the digital field. We picked out some insurtechs that really stood out for us, with exemplary user experience, unique offerings and a memorable company presence.

Insurtechs with a great user experience

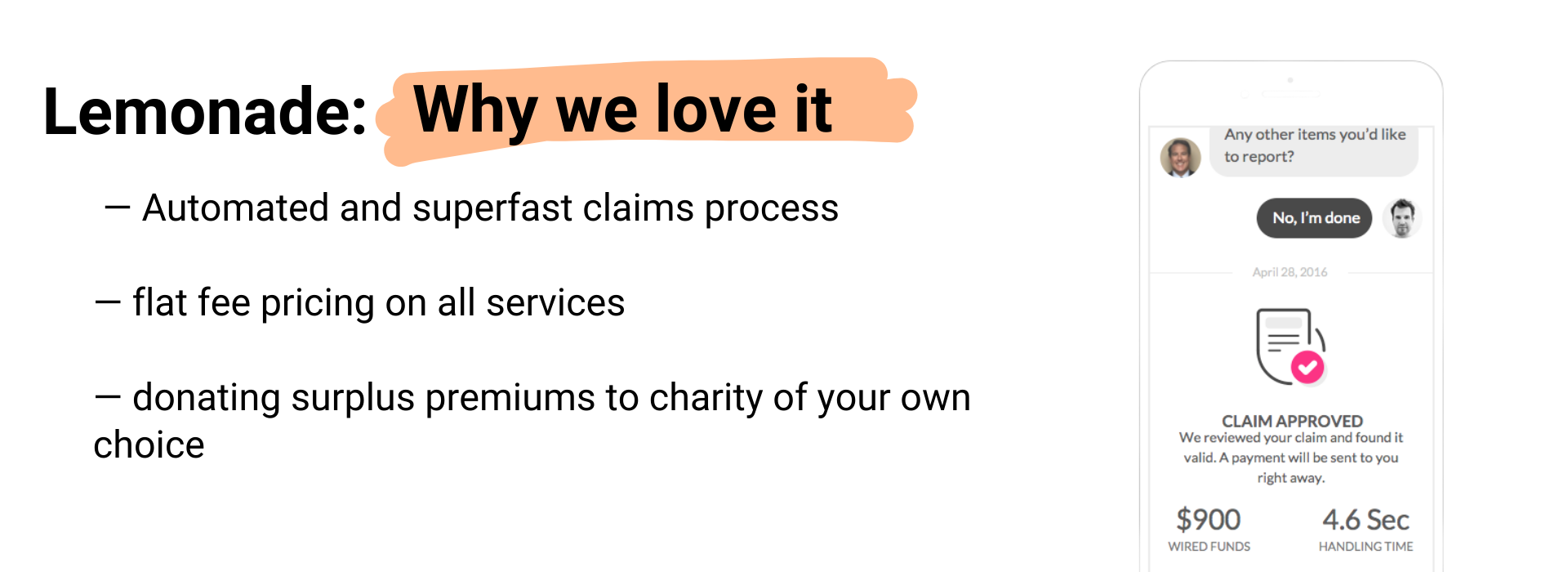

Lemonade

Lemonade is a U.S. based insurance company that offers renters’, homeowners’ and pet insurance. They stand out from the crowd with their promise of “90 seconds to get insured, 3 minutes to get paid” by utilising multiple algorithms for claims handling and underwriting automation. About 30% of all Lemonade claims are handled by the chatbot AI Jim, while more complex cases are sent to human representatives. They are also the only insurance company so far to take a flat fee and donate all surplus premiums to charity, compared to competitors who are known to withhold coverage to boost their profits.

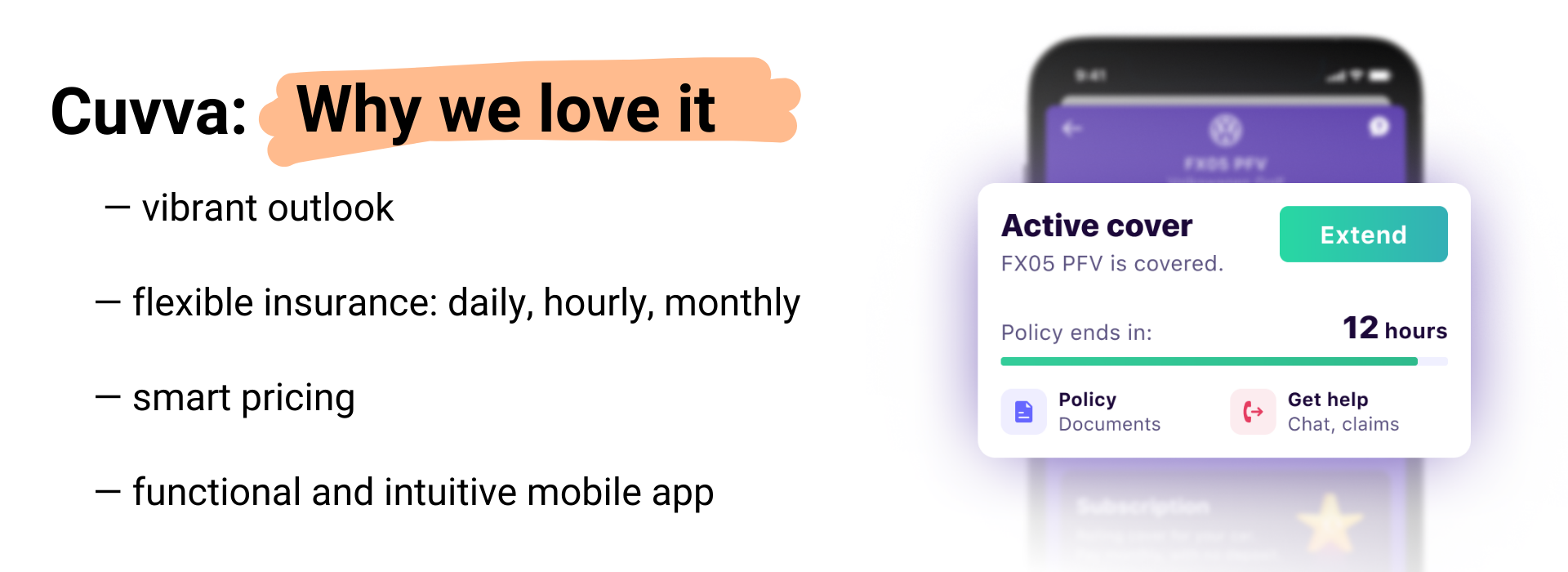

Cuvva

“Cuvva - car insurance that isn’t sh*t”. Bold, right? Wait till you see the vibrant Cuvva advertisement. Gone are the days of insurance companies that rely on stock images with smiley faces that are supposed to ‘speak trust’. Digital-savvy customers look for brands that not only answer their needs, but who also have the same identities. Cuvva is car insurance ‘for the no-strings-attached types’. From hourly, daily or monthly subscription and no cancellation fees, they are made for fast-paced communities. Through the Cuvva mobile app, users can manage all their policies, upload all necessary documents through the license scanner, and get notifications for ending policies. Cuvva is also among the few that offer smart insurance pricing - the better you drive, the less you pay for your insurance.

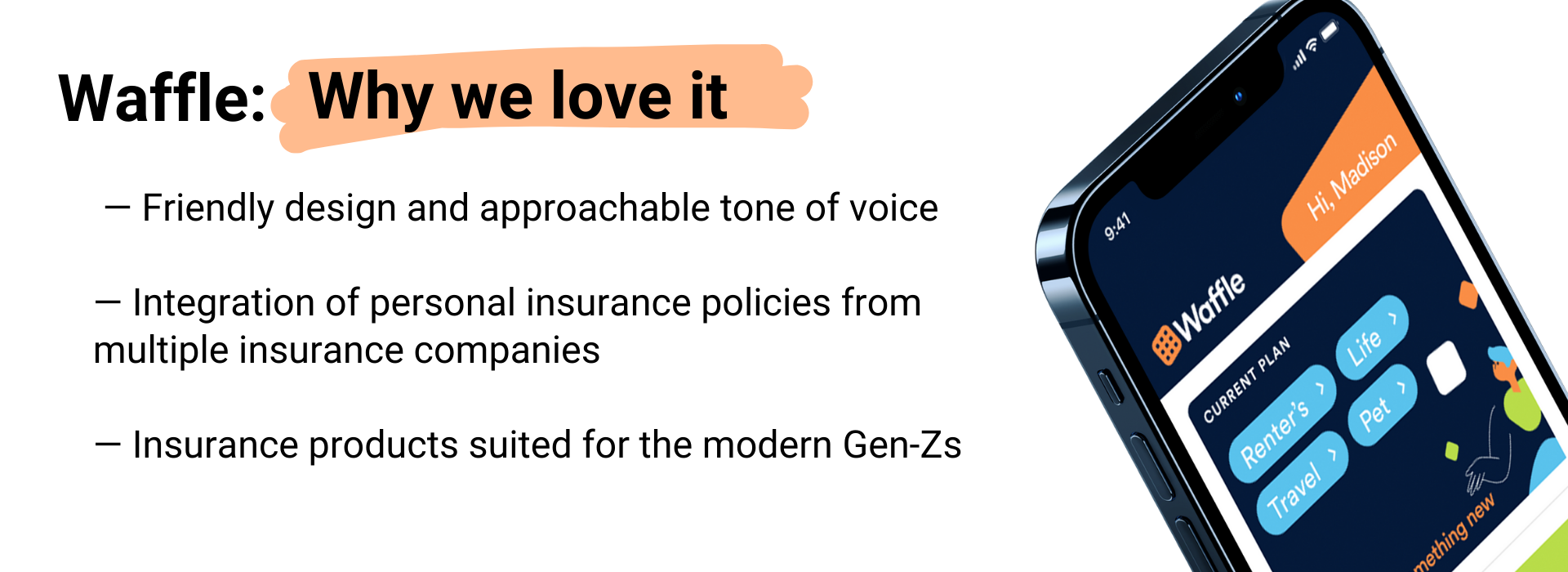

Waffle Insurance

For many types of insurance policies, insurance equals hassle, and this is exactly Waffle’s selling point. Through playful tone, pastel colours and simplified processes, they are bringing a human touch to the digital insurance experience. Not to mention the fact that their insurance products are perfectly suited to the modern Gen-Zs - they can choose between cyber, renters’, pet and travel insurance (or all of them at the same time). Waffle also allows users to integrate their existing personal insurance policies from multiple companies and access all of them in one, easy-to-access portal.

Circulo Health

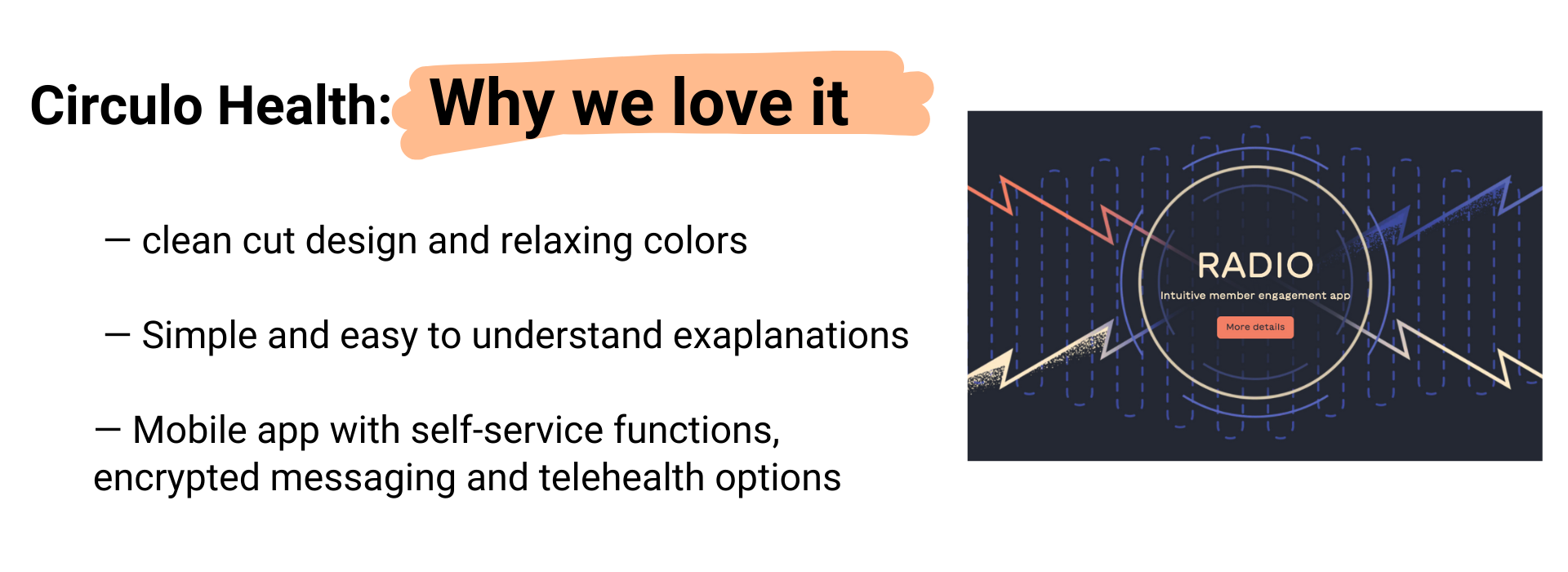

Not all insurance should be instagrammable, though. Circulo Health, an Ohio-based insurtech startup for the Medicaid population, that aims to “bring bold new approaches and internet-scale technology” to Medicaid members, has a more simplified, sophisticated touch. What’s noteworthy about the startup is its connections with Olive, an artificial intelligence unicorn that automates high-volume administration tasks for healthcare organisations. Although Circulo is still in its early days and currently has just a sparse homepage, it received $50 million funding and is expected to open its doors pretty soon. The Radio app is expected to have self-service handling, encrypted messaging between providers and members, as well as telehealth options.

You’re an insurer. Do you need a mobile app?

To answer your question briefly, it depends. Having an insurance mobile app is not going to solve all your problems, especially if there are some pressing ones within the organisation. We’ve already covered some ground rules for starting an insurer’s digital journey, and they mostly point towards a proper strategy and a ‘digital mindset’. Because the truth is, if all your claims and processes are still relying on legacy systems and siloed departments, an app is not going to fix that. If you’ve already done that, a possible next step would be analysing your customer channels and implementing an omnichannel insurance experience. In any case, the insurtechs we covered so far should serve as an inspiration on ways you could go with your digital offerings.

Ready to shake things up?

Hopefully we made a strong case of the lessons traditional insurance companies can take from insurtechs about their customer experiences.We are strong believers that technology can be of use for both insurance customers and providers,and we’re looking for partners who share our belief. If you dream about shaking up the health insurance industry for the better, reach out to us.